Budgeting, Accounting and Reporting System (BARS)

GAAP

For Cities, Counties and Special Purpose Districts

Source: https://sao.wa.gov/bars-annual-filing/bars-gaap-manual

Last updated on July 10, 2026

The BARS Manual is currently updated for all applicable GASB Statements required for fiscal year 2025 reporting. This update occurred on December 1, 2025.

The annual report for the fiscal year ended December 31, 2025, is required by Saturday, May 30, 2026 (RCW 43.09.230).

The Budgeting, Accounting and Reporting System (BARS) Manual prescribes accounting and reporting for local governments in accordance with RCW 43.09.200. Its purpose is to provide (1) uniform accounting and financial reporting to allow for meaningful use and comparison of financial data; (2) accounting and reporting instructions as a resource for local government managers; and (3) a consistent framework for financial reporting to intended users, including managers, governing bodies, granting and regulatory agencies, the state Legislature, and the general public.

The manual is maintained by the State Auditor's Office with input from the Local Government Advisory Committee. It is continuously reviewed to ensure prescription and instructions remain current and appropriate to meet the needs of intended users. Accounting and reporting guidance incorporates analysis of generally accepted accounting principles (GAAP) published by the Governmental Accounting Standards Board as they become effective.

This manual is designated for all GAAP cities, counties and special purpose districts.

Governments should refer to the source standards when researching or early implementing GASB Statements, by visiting https://gars.gasb.org/.

View the detailed Alerts and Changes tab for current year updates.

In need of technical assistance? Visit the Help Desk.

In accordance with the Americans with Disabilities Act, we will make this document available in alternative formats. For more information, please contact our Office at (564) 999-0950, TDD Relay at (800) 833-6388, or email our webmaster at webmaster@sao.wa.gov.

BARS Account Exports

In this section, governments can access a report providing information on the allowability of BARS codes in fund types as well as export a chart of accounts specific to a government type.

BARS Codes to Fund Type

BARS codes may be restricted for use in the annual report filing system. The following matrix “Codes to Funds” identifies which fund group(s) that each active BARS code may be reported in.

Download FY2025 Codes to Funds here. Codes are as of December 1, 2025

Note: It is recommended to use this matrix in conjunction with the government specific BARS Account Export provided below.

BARS Account Export

Download a government specific BARS Chart of Accounts in the export box at the bottom of this page.

Your annual report requires seven digits for all account codes however, their display in the chart of accounts export varies. The expenditure or expense accounts are presented in the export without object codes. Object codes will need to be added to the BARS Code to complete the required seven digits for the annual report. Additional details about object codes are available in the BARS Manual 1.4, Object Codes. Reporting at the sub object level is not required.

How to use the BARS Account Export

Select a government type

The government type selection will limit the BARS accounts that are applicable to the selected government type. If all is selected, the export will include BARS accounts for all government types.

Select basis of accounting

The basis of accounting selection will limit the BARS accounts that are applicable to the basis of accounting selected (GAAP or Cash). If all is selected, the export will include all the BARS codes regardless of their applicability to a specific basis.

Select export type

The Excel option provides a spreadsheet which you can format.

The PDF is formatted to highlight the different categories of account codes and for printing. For display purposes, the account codes contain decimal points which should be excluded in your annual report.

Select a reporting level

Above and Prescribed option includes all the accounts, including the accounts in which other codes are rolled up into for category presentation. These above prescribed codes are not valid for reporting; however they provide detailed information on the category of the codes. This listing also provides the Prescribed accounts, which are the required accounts for annual report filing.

The Prescribed option includes only the accounts which are the valid BARS account codes for annual report filing.

1 Charts of Accounts

1.1.2 Account Structure

1.1.2.10 All BARS codes are required to be seven-digits for reporting purposes on the Schedule 01. Local governments may include additional digits within their internal account structure, such as fund numbers and added digits for tracking details. If a different system of numbers is used for internal accounting, it must contain equivalent detail throughout the budget, accounting, and reporting process.

See BARS 3.1.1, Fund Accounting and Fund Types for the structure of fund numbers, which are separate from the required structure of BARS codes.

1.1.2.20 The seven-digit BARS code structure has the following components:

First digit

3 (three) represents beginning fund balances/net position, revenues, and other financing sources.

5 (five) represents ending fund balances/net position, expenditures/expenses, and other financing uses.

Second and third digits

Revenue – represents the source (origin or originating category) of revenues. These digits are always prescribed and required for reporting on the Schedule 01.

Expenditures/Expenses – represents the different functions and activities for which the expenditures/expenses are supporting.

Fourth and fifth digits

Revenue – represents further details for specific types of revenues within a particular source.

Expenditure/Expense – represents further details for specific elements and sub-elements of activities related to the particular function and activity.

Sixth and seventh digits

Revenue – these digits are generally not defined and are represented as zeros. When these digits are represented as zeros, they are available for customization by the local government. However, there are exceptions to this rule. The BARS codes within the 330 series prescribe all seven digits and cannot be customized. Local governments should be aware that as the BARS manual is updated, these digits may be assigned for specific purposes.

Expenditure/Expense – represents the object code, which identifies the specific type of items that support the activity or function. For additional information on object codes, please see BARS 1.4, Object Codes.

1.1.2.30 The tables below provide an overview of the major categories of BARS codes. For the complete listing of all BARS codes with their full definitions, go to BARS Account Export.

Beginning and Ending Fund Balance/Net Position

|

300 |

|

Beginning Fund Balance/Net Position |

|

|

308 |

Beginning Fund Balance/Net Position |

|

500 |

|

Ending Fund Balance/Net Position |

|

|

508 |

Ending Fund Balance/Net Position |

Major categories of revenues by source

|

310 |

Taxes |

|

|

|

311 |

Property Tax |

|

|

313 |

Retail Sales and Use Taxes |

|

|

316 |

Business and Occupation Taxes |

|

|

317 |

Excise Taxes in Lieu of Property Tax |

|

|

318 |

Other Taxes |

|

320 |

|

Licenses and Permits |

|

|

321 |

Business Licenses and Permits |

|

|

322 |

Non-Business Licenses and Permits |

|

330 |

|

Intergovernmental Revenues |

|

|

331 |

Federal Direct Awards |

|

|

332 |

Federal Other Award Revenues |

|

|

333 |

Federal Indirect Awards |

|

|

334 |

State Grants, Awards, and Other Contributions |

|

|

335-336 |

State Shared Revenues, Entitlements and Impact Payments |

|

|

337 |

Local Awards, Entitlements, Tribal Government Distributions, and Other Payments |

|

340 |

|

Charges for Goods and Services |

|

|

341 |

General Government |

|

|

342 |

Public Safety |

|

|

343 |

Utilities |

|

|

344 |

Transportation |

|

|

345 |

Natural and Economic Environment |

|

|

346 |

Social Services |

|

|

347 |

Culture and Recreation Fees |

|

|

348 |

Internal Service Funds Sales and Services |

|

350 |

|

Fines and Penalties |

|

|

351 |

Superior Court - Felony/Misdemeanor Penalties |

|

|

352 |

Civil Penalties |

|

|

353 |

Civil Infraction Penalties |

|

|

354 |

Civil Parking Infraction Penalties |

|

|

355 |

Criminal Traffic Misdemeanor Fines |

|

|

356 |

Criminal Non-Traffic Fines |

|

|

357 |

Criminal Costs |

|

|

359 |

Non-Court Fines and Penalties |

|

360 |

|

Miscellaneous Revenues |

|

|

361 |

Interest and Other Earnings |

|

|

362 |

Rents and Leases |

|

|

367 |

Contributions and Donations from Nongovernmental Sources |

|

|

368 |

Special Assessments |

|

|

369 |

Other Miscellaneous Revenues |

|

370 |

|

Proprietary Funds - Other Revenue (Expense) and Capital Contributions |

|

|

371 |

Share in the Joint Venture Income (Increase/Decrease) |

|

|

372 |

Insurance Recoveries |

|

|

373 |

Gains (Losses) on Capital Assets |

|

|

374 |

Capital Contributions-State/Local/Direct Federal |

|

|

375 |

Capital Contributions-State/Local/Indirect Federal |

|

|

379 |

Capital Contributions |

Other Increases and Financing Sources

|

380 |

|

Other Increases in Fund Resources |

|

|

385 |

Special or Extraordinary Items |

|

|

386 |

Court Remittances |

|

|

388 |

Other Increases in Fund Balance |

|

|

389 |

Custodial Activities |

|

390 |

|

Other Financing Sources |

|

|

391 |

Debt Issued |

|

|

392 |

Premiums on Bonds Issued |

|

|

393 |

Refunding Long-Term Debt Issued |

|

|

395 |

Disposition of Capital Assets |

|

|

397 |

Transfers-In |

|

|

398 |

Insurance Recoveries |

Major functions of expenditures

|

501 |

|

Proprietary Funds - Depreciation, Depletion, Amortization |

|

510 |

|

General Government |

|

|

511 |

Legislative Activities |

|

|

512 |

Judicial Activities |

|

|

513 |

Executive Activities |

|

|

514 |

Financial, Recording and Election Activities |

|

|

515 |

Legal Services |

|

|

517 |

Employee Benefit Programs |

|

|

518 |

Centralized/General Services |

|

|

519 |

Risk Management Services |

|

520 |

|

Public Safety |

|

|

521 |

Law Enforcement Activities |

|

|

522 |

Fire and Emergency Medical Activities |

|

|

523 |

Detention/Correction Activities |

|

|

524 |

Protective Inspection Services |

|

|

525 |

Disaster Services |

|

|

527 |

Juvenile Services |

|

|

528 |

Dispatch Services |

|

530 |

|

Utilities |

|

|

531 |

Storm Drainage Utilities |

|

|

532 |

Television/Cable/Internet Utilities |

|

|

533 |

Electric/Gas Utilities |

|

|

534 |

Water Utilities |

|

|

535 |

Sewer/Reclaimed Water Utilities |

|

|

536 |

Cemetery |

|

|

537 |

Solid Waste Utilities |

|

|

538 |

Combined Utilities |

|

|

539 |

Irrigation/Reclamation Utilities |

|

540 |

Transportation |

|

|

|

541 |

Roads/Streets modified approach only - condition rating preservation |

|

|

542 |

Roads/Streets Ordinary Maintenance |

|

|

543 |

Roads/Streets General Administration and Overhead |

|

|

544 |

Roads/Streets Operations |

|

|

545 |

Roads/Streets Extraordinary Operations |

|

|

546 |

Airports and Ports |

|

|

547 |

Transit, Railroads and Other Transportation Systems |

|

|

548 |

Public Works – Centralized Services |

|

550 |

Natural and Economic Environment |

|

|

|

551 |

Public Housing Services |

|

|

552 |

Employment Opportunity |

|

|

553 |

Conservation |

|

|

554 |

Environmental Services |

|

|

557 |

Community Services |

|

|

558 |

Community Planning and Economic Development |

|

559 |

Property Development |

|

|

560 |

|

Social Services |

|

|

561 |

Hospitals, Assisted Living and Convalescent Facilities |

|

|

562 |

Public Health Services |

|

|

563 |

Coroner/Medical Examiner |

|

|

564 |

Mental Health Services |

|

|

565 |

Welfare/Veterans Services/Services for Disabled/Homeless Services/Domestic Violence |

|

|

566 |

Chemical Dependency Services |

|

|

567 |

Children Services |

|

|

568 |

Developmental Disabilities Services |

|

|

569 |

Aging and Disability Services |

|

570 |

|

Culture and Recreation |

|

|

571 |

Educational and Recreational Activities |

|

|

572 |

Libraries |

|

|

573 |

Cultural and Community Events |

|

|

575 |

Cultural and Recreational Facilities |

|

|

576 |

Park Facilities |

|

598 |

|

Proprietary Funds - Miscellaneous Expenses |

Other Decreases and Financing Uses

|

580 |

|

Other Decreases in Fund Resources |

|

|

585 |

Special or Extraordinary Items |

|

|

588 |

Other Decreases in Fund Balance |

|

|

589 |

Custodial Activities |

|

590 |

|

Debt Expenditures, Capital Outlays, and Other Financing Uses |

|

|

591 |

Debt Repayment |

|

|

592 |

Interest and Other Debt Service Costs |

|

|

593 |

Advance Refunding Escrow |

|

|

594 |

Capital Expenditures |

|

|

595 |

Roads/Streets and Related Infrastructure: Improvements and New Construction Projects |

|

|

596 |

Issuance Discount on Long-Term Debt |

|

|

597 |

Transfers-Out |

|

|

599 |

Payments for Refunded Debt |

Balance sheet codes for Schedule 01 reporting

|

800 |

|

Balance Sheet Accounts |

|

|

810 |

Cash, Cash Equivalents and Investments |

|

|

820 |

Other Current Assets |

|

|

830 |

Noncurrent Assets |

|

|

840 |

Deferred Outflows |

|

|

850 |

Current Liabilities |

|

|

860 |

Noncurrent Liabilities |

|

|

870 |

Deferred Inflows |

1 Charts of Accounts

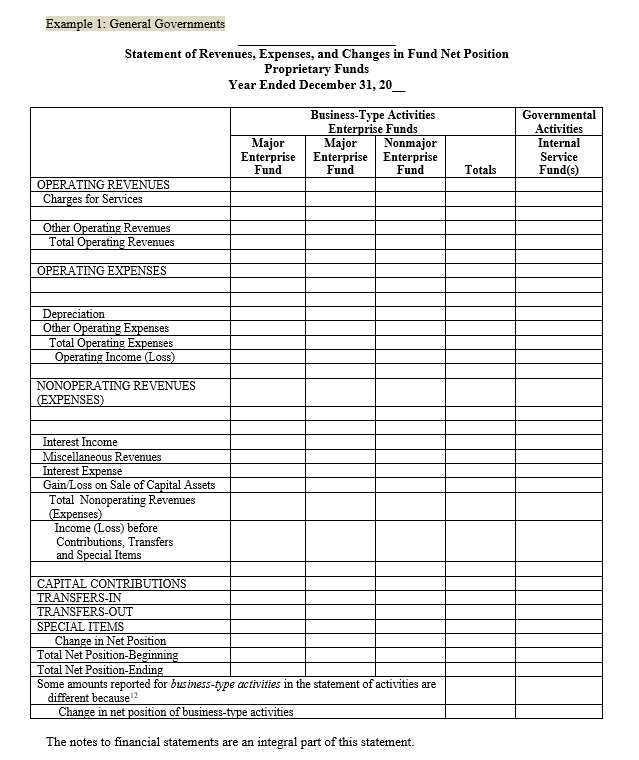

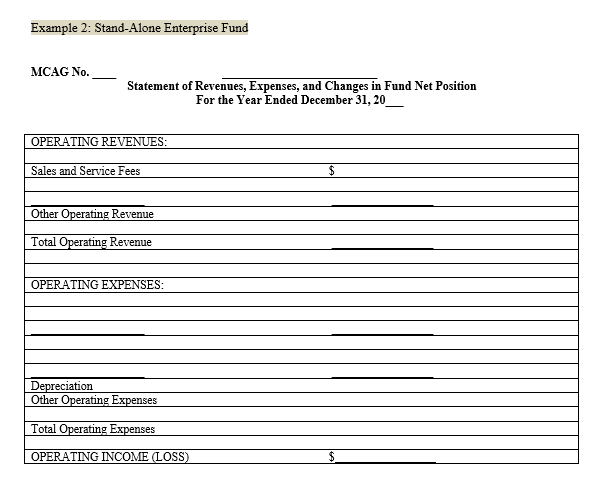

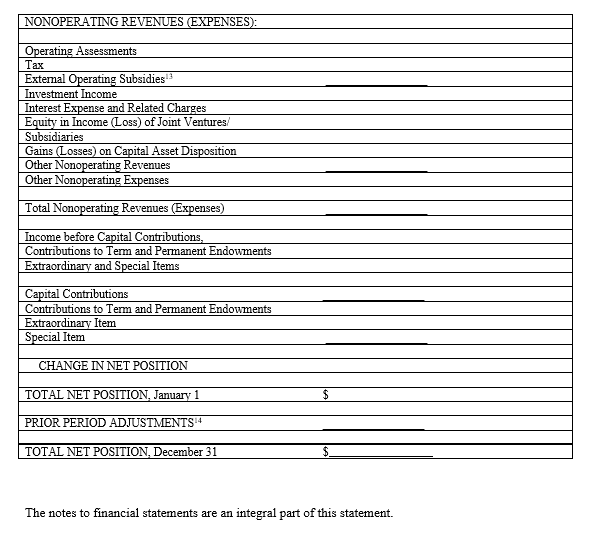

1.5 Determining Operating/Nonoperating Revenues/Expenses in Proprietary Funds

1.5.10 The Proprietary Fund Statement of Revenues, Expenses, and Changes in Net Position requires governments to distinguish operating revenues and expenses from non-operating revenues and expenses. Several BARS codes have been defined as operating or non-operating, however some BARS codes can be either operating or nonoperating. The following matrix “Operating vs. Non-operating” identifies the classifications as they are reflected in the annual filing system. BARS codes that can be either operating or non-operating will need to be allocated in the annual filing system. The governments may use the matrix as a guide for the preparation of their statement of revenues, expenses and changes in net position (operating statements).

Download the Operating vs. Non-Operating matrix here.

1.5.20 Because operating revenues/expenses are not authoritatively defined in the accounting literature, there is no assurance that the usage of these term is standardized. Since the State Auditor’s Office is required to provide comparative statistics for all local governments, the Office made some decisions which are based on a reasonable extension of existing standards that do not have direct citations in GAAP literature.

1.5.30 GASB Statement 34, Basic Financial Statements - Management Discussion and Analysis - for State and Local Governments, paragraph 436, states that there are two criteria to consider when defining revenues and expenses as operating: (1) does the revenue/expense result from the fund’s principal purpose, and (2) is the revenue/expense allowed to be considered operating on the statement of cash flows [again, this is a guideline, not a requirement].

1.5.40 The operating nature of revenue is derived from the source of the revenue NOT its purpose. The fact that the revenue supports the operations does not impact its classification which again refers to the revenue origin.

1.5.50 GASB Cod. Sec. 2200 "Annual Comprehensive Financial Reporting" requires proprietary fund revenues to be reported by major source (net of discounts and allowances). Codification further requires proprietary to distinguish between operating and nonoperating revenues and expenses.

1.5.60 The objective of the distinction of nonoperating and operating is to display the extent to which operating expenses are covered by revenues generated by principal ongoing operations (2015-1 Comprehensive Implementation Guide, Question 7.73.4). For example, interest is operating revenue if the principal activity of the fund is to provide loans to generate income. The ongoing principal operation is determined by the purpose of the individual enterprise fund.

1.5.70 GASB Statement 34, paragraph 102, indicates that one consideration for defining operating revenues and expenses is how individual transactions would be categorized for cash flows from operating activities in the cash flows statement. Operating revenues are generally those that enter into the determination of the operating income. This is a guideline, not a requirement. [See reference to footnote 42 on page 36, after paragraph 104 of GASB Statement 34.]

1.5.80 According to the GASB Cod. Sec. 2450 "Cash Flows Statements" operating cash flows category would exclude most revenues that considered to be non-exchange and exchange-like transactions and financing and investment-related revenues/expenses, including:

1.5.90 Generally governments should record the following proprietary fund operating revenues:

1.5.100 Taxes (310)

GAAP governments are not created to generate tax revenue. Taxes are not comparable to charges for services, as they are result of statutory authority only. It does not matter how specific the tax is regarding its use or purpose. Property and other taxes should be always reported as nonoperating revenue in proprietary fund statements.

Licenses and Permits (320)

Licenses and permits are generally exchange or exchange-like transactions. Usually the price of paying the cost of issuing a license or permit amounts to the cost necessary to process that permit. Permit may be considered operating if it is an integral component of the enterprise funds’ primary operations, and if it is considered operating from the perspective of the cash flows statement. Another example of permits and licenses being an operating revenue would include a permit fee collected by an enterprise fund whose purpose is to issue permits.

Grants/Intergovernmental Revenues (330)

Operating grants and contributions (both received and made) that are not restricted for capital purposes [these are reported as capital contributions] are excluded from an operating category since these are result of non-exchange transactions. Capital grants are always excluded. GASB Cod. Sec. 2450 specifically includes grants or subsidies provided to finance operating deficits in the noncapital financing category, rather than the operating activities category. Based on that guidance, annual operating grants and subsidies should be reported as nonoperating revenues.

For example grants reported in a transit enterprise funds should not be reported as operating revenue but, rather, as non-operating revenue or as capital contributions [reported separately after non-operating revenues and expenses]. This is because the grants are funding the deficit and are not received because the state/feds are paying on-behalf of riders or passengers.

However, grants that are essentially the same as a contract for services, should be reported as operating revenues. Grants primarily benefit particular grantee furthering grantees own purpose or program. Grantor involvement is limited to administration and monitoring. It also benefits the grantor own program directly (e.g., federal government providing Medicare by law). This is in substance an exchange transaction.

Operating grants (vs. capital) are intended to finance operations, but they are not a result of operations.

Charges for Goods and Services (340)

If these revenues are result of the governments’ principal operations, they should be coded as operating.

Fines and Penalties (350)

GASB Cod. Sec. N50 "Nonexchange Transaction" classifies fines as imposed non-exchange transactions, which excludes them from the operating revenue category. They should be reported as nonoperating revenues.

Miscellaneous Revenues (360)

Majority of the miscellaneous revenues are considered nonoperating unless they are directly related to the government principal operation; if so, then they should be coded in the functional area. For example, interest revenue should be reported as nonoperating. They can be operating only if proprietary fund’s principal operation is to provide loans. We believe there are no governments in the Washington State established only for this purpose.

Also, rentals and leases are all nonoperating unless the rental is directly related to the principal operation, (a port district that primarily functions as marina, should code all non-marina rentals as nonoperating, etc.).

Service-type special assessments are exchange or exchange-like transactions which affect only those who directly benefit from a given service. Unlike the capital-type special assessments which should be reported as capital contributions, the service-type assessments can be reported as operating revenues if they are directly related to the principal operations of the government.

The immaterial amounts of all other revenues, not specifically listed in the BARS manual, should be coded either to 36991, Miscellaneous Other or 36992, Miscellaneous Other Nonoperating depending on their relationship to the governments’ primary operations.

1.5.110 Expenses

Since there is no authoritative definition what constitutes the operating expenses, each government must disclose the basis on which it separates operating from nonoperating expenses. This distinction should allow to demonstrate the extent to which the government is able to recover from its customers the cost of producing goods and providing services. So, the cost of goods sold and services provided constitute operating expenses.

1 Charts of Accounts

1.6 Memorandum Accounts in Proprietary Funds

1.6.10 Introduction

For GAAP proprietary funds, local governments are required to report financial activity related to debt and capital assets, which are not reported in the operating statement. This activity is required to be reported on the Schedule 01 using memorandum accounts. The collection of this data is necessary for the State Auditor’s Office to produce comparative statistics, as required by state law (RCW 43.09.230).

See BARS 4.8.1, Revenues/Expenditures/Expenses (Schedule 01) for instructions on preparing the Schedule 01.

1.6.20 Capital Assets

For GAAP proprietary funds, when a capital asset is purchased, no expense/outflow is recorded on the on the Statement of Revenues, Expenses, and Changes in Net Position. The use of memorandum accounts allows the local government to accurately report the amount paid for capital related items. The memorandum accounts for capital outlay are listed in the table below:

|

594 |

Capital Expenditures/Expenses |

|

595 |

Road/Streets and Related Infrastructure: Improvements and New Construction Projects |

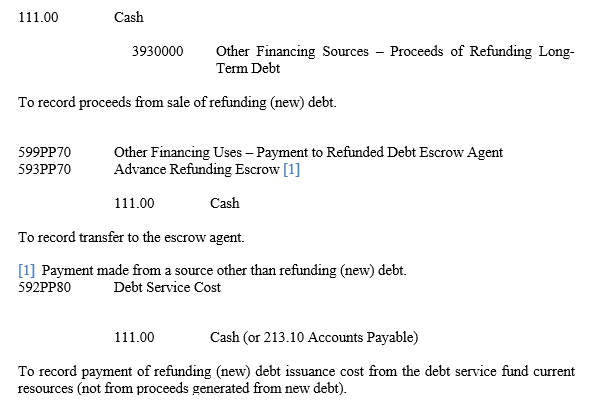

1.6.30 Debt

For GAAP proprietary funds, when debt is issued, no revenue/inflow is recorded on the Statement of Revenues, Expenses, and Changes in Net Position. The same concept applies when debt is paid in a proprietary fund, no expense/outflow is recorded on the operating statement.

The use of memorandum accounts reports the amount of debt issued and paid, which ensures accurate and complete financial reporting on the Schedule 01. The debt memorandum accounts must be used for all debt and financings, including leases and SBITAs. These accounts are listed in the table below:

|

391 (Debt Issued/Bond Proceeds) |

591 (Redemption of Debt) |

|

392 (Premiums on Bonds Issued) |

593 (Advance Refund Escrow) |

|

393 (Refunding Long-Term Debt Issued) |

596 (Issuance Discount on Long-Term Debt) |

1.6.40 Annual Filing System

For GAAP proprietary funds, the memorandum accounts are required to be reported and are used for informational purposes only. These accounts are not included in the filing system calculation for the $1,000 balancing requirement and are not included in the system calculation for total expenditures.

When completing the Schedule 01, the 591 and 594 BARS codes are required to be reported in all GAAP proprietary funds, even if the amount is $0. If these codes are omitted, it will result in a required error. If $0 is reported to the 591 and 594 BARS codes, it will result in a warning error, which is meant to encourage local governments to double-check that reporting $0 for debt and capital payments is accurate. If the amount is truly $0, the warning error may be disregarded, and it will not prevent the submission of the report.

For additional guidance on errors and how to correct them in the annual filing system, see the Error Guide here: BARS & Annual Report Filing FAQs.

1 Charts of Accounts

1.4 Object Codes

00 Depreciation, Amortization, Other Decreases in Fund Resources and Transfers-Out

Use this category with the accounts 501, 581, 582, 585, 586, 588, 589, and 597.

10 Salaries and Wages

Use this object code for the gross amounts paid for personal services rendered by employees in accordance with the rates, hours, terms and conditions authorized by law or stated in employment contracts. This category also includes overtime, hazardous duty or other compensation construed to be salaries and wages. Governments may subdivide this account as necessary for detailed local purpose reporting (i.e., regular pay, overtime pay, sick pay (employee related), sick pay (non-employee related), vacation pay, shift differential, and other taxable compensation).

Personal services do not include fees and out-of-pocket expenditures for professional or consultant services performed on assignments. Such services are properly classified as object code 40.

20 Personnel Benefits

Use this object code for the employer’s share of benefits provided to employees, in addition to compensation, that are part of the conditions of current or past employment. Governments may subdivide this account as needed for detailed local purpose reporting (i.e., health/vision/dental insurance, unemployment compensation payments and/or premiums, Social Security, Medicare taxes, uniforms, pension, and workers' compensation).

Payments for pay-as-you-go health and welfare plans, or pension/OPEB plans would be coded to personnel benefits. Payments to fund either a self-insurance fund for health and welfare type benefits or a pension/OPEB fund would also be coded to personnel benefits, then subsequent payment from the self-insurance funds and non-fiduciary pension/OPEB funds for all claims would use object code 40 for the payments.

30 Supplies for Consumption and Resale

Use this object code for:

40 Services and Pass-Through Payments

Use this object code for professional and technical services which are provided by other governments (federal, state, local), other funds, or by private entities as well as for pass-through payments as described below.

Services include but aren’t limited to the following examples:

Pass-through payments include eligible intergovernmental payments, contributions and grants that the government has received from federal, state, or other local governments and are passed through to other entities.

60 Capital Outlays

Use this object code for expenditures related to the purchase or construction of assets considered capital according to the government’s capitalization threshold policy. This object code should be used only with accounts 594 and 595.

Include expenditures related to acquisition of, rights to, or additions to capital assets, including incidental costs such as legal, appraisal and brokerage fees, land preparation and demolishing buildings, fixtures and delivery costs. This category includes purchases and construction of major capital assets which are purchased or constructed by the external party. Assets constructed or fabricated by the municipality should be classified under other object codes; i.e., wages under object code 10, materials, small tools and minor equipment under object code 30, etc. Include:

70 Debt Service – Principal

Use this object code with codes 591, 593, 594 (cash basis only), 596 and 599. Include general obligation, revenue, special assessment bonds, long-term leases/SBITA, installment purchases, anticipation and other notes, anticipation warrants, contracts, intergovernmental loans, other debt, LOCAL program payments, etc.

80 Debt Service – Interest and Issuance Costs

Use this object code with codes 592, 593, 594 (cash basis only) and 599. Include interest on short and long-term external debt, interest on interfund debt, interests on debt to joint ventures and affiliates, LID assessments, interest on intergovernmental debt, leases, interest paid on overdue taxes (RCW 84.69.070), debt issuance and other debt service costs.

1 Charts of Accounts

1.2 Optional - General Ledger Accounts

1.2.10 The specific account numbers contained here are not prescribed, with an exception for selected liabilities accounts which are required to be reported on the Schedule of Liabilities (Schedule 09). This general ledger has been carefully designed to meet several needs.

1.2.20 First, the accounts provide for identification of assets, deferred outflows, liabilities, deferred inflows and fund balances/net position that any local government fund might acquire. Throughout the general ledger, the fourth or fifth and subsequent digits have been left for local governments to use in establishing more detailed breakdowns where needed.

1.2.30 Second, the general ledger has been designed to permit logical summarization of the detailed accounts at various levels. The table below illustrates in detail the structure of the general ledger.

1.2.40 Third, the comprehensiveness of the general ledger combined with the uniform summarization outlined above is designed to make the preparation balance sheets/statement of net position a simple matter of extracting the balances at the same level for all the funds of a government. The headings on the attached chart identify which digits to sort or summarize by for reporting purposes. The presentation of a balance sheet/statement of net position is structured in similar manner as the general ledger accounts as shown in the attached chart.

1.2.50 The following excel file provides the list of optional general ledger accounts. The “GL Accounts” tab provides account titles and their corresponding account number. The “GL Accts w Descriptions” tab provides account titles and their corresponding account number along with account descriptions.

Download the excel workbook here: General Ledger Accounts

2 Budgeting

2.4 Budget Compliance

2.4.1 Introduction

2.4.1.10 A budget is a legal document that forecasts the financial resources of a government and authorizes the spending of those resources for a fiscal period. At a minimum, local governments’ budget must meet the requirements of Washington state law and the State Auditor’s Office. The SAO does not prescribe how to budget or what a budget should look like. The adopted budget should be of sufficient detail to be meaningful and meet the intention of the law. The SAO considers budgets showing revenues and expenditures at the legal fund level to be the minimum acceptable level of detail.

2.4.1.20 Budgeting is more than just an activity to satisfy state law. It is a sophisticated process of strategic planning, communication and policy development resulting in a detailed plan of operations for allocating and monitoring the use of limited resources among various competing demands. Teaching how to budget is outside the scope of the BARS. However, there are many educational resources available to local governments, such as the Municipal Research and Services Center (mrsc.org) and the Government Finance Officers Association (gfoa.org).

2.4.1.30 Glossary of budgetary terms:

Annual/biennial appropriated budget – A fixed budget adopted for the government’s fiscal period. The appropriated budget was traditionally used to determine a government’s property tax levy, and a ceiling on expenditures was made absolute so that the expenditures of a government unit would not exceed its revenues. This budget was also historically a balanced budget, estimated revenues equaling appropriations. The appropriated budget is still used to set tax levies and some budget statutes still require balanced budgets, but it is more generally used to authorize a specific amount of expenditures regardless of whether estimated resources meet or exceed that amount. Appropriated budgets are required by statute in cities (Chapter 35.32A RCW, Chapter 35.33 RCW and Chapter 35A.33 RCW), counties (Chapter 36.40 RCW), and most other local governments in Washington State. These budgets are also called legal budgets, adopted budgets, or formal budgets. The appropriated budgets should be adopted by ordinance or resolution.

Appropriation – The legal spending level authorized by a budget ordinance or resolution. Spending should not exceed this level without prior approval of the governing body.

Capital improvement budget – Consists of two elements: the annual/biennial portion of capital projects and annual/biennial appropriations for the purchase, construction or replacement of major fixed assets in the current fiscal period.

Comprehensive budget – A government-wide budget that includes all resources the government expects and everything it intends to spend or encumber during a fiscal period. The comprehensive budget contains annual/biennial appropriated budgets, the annual/biennial portion of continuing appropriations such as the capital improvement projects, debt amortization schedules, and grant projects, flexible budgets and all non-budgeted funds.

Continuing appropriation – A fixed budget which authorizes expenditures for a fiscal period that differs from the government’s fiscal year, such as capital projects, debt issues, grant awards, and other service projects. These expenditures require an ordinance or resolution to authorize the project, establish the assessment roll, adopt the debt amortization schedule, or accept the grant award. Such ordinances or resolutions set an absolute maximum or ceiling on the expenditures, but the time period for incurring expenditures does not coincide with the government’s fiscal year; it may even cover several years. The major difference between annual/biennial appropriated budgets and continuing appropriations is that the latter do not lapse at fiscal period end; this implies that no legislative action is required to amend the annual/biennial portion of a continuing appropriation, unless the total authorized expenditures would exceed the entire appropriation.

Encumbrances – Commitments related to unperformed (executory) contracts for goods or services should be utilized to the extent necessary to assure effective budgetary control and to facilitate cash planning. Encumbrances outstanding at year end represent the estimated amount of expenditures ultimately to result if unperformed contracts in process are completed; they do not constitute expenditures or liabilities.

Final amended budget – The original budget adjusted by all reserves, transfers, allocations, supplemental appropriations, and other legally authorized legislative and executive changes applicable to the fiscal year, whenever signed into law or otherwise legally authorized.

Fixed budget – Those budgets which set an absolute maximum or ceiling on the expenditures of a particular fund, department, or other specific category. A fixed budget can be either an annual/biennial appropriated budget or a continuing appropriation. Fixed budgets must be adopted by ordinance or resolution, either for the government’s fiscal period or at the outset of a service project, debt issue, grant award, or capital project.

Flexible budgets – Are usually regarded as managerial tools, which do not set a ceiling on expenses or expenditures but establish a plan for them at various levels of service. They are especially appropriate for the day-to-day operations of a public utility where it is essential to plan fluctuations in the demand for services and where revenues will automatically increase with demand, so that a balanced budget does not depend on establishing a ceiling for expenses.

Operating budget – Presents the estimated expenditures and available resources necessary to provide the services for which the government was created. An operating budget will contain flexible budgets and fixed budgets; the fixed budgets will include annual/biennial appropriations for services and the annual/biennial portion of continuing appropriations for debt service and for service projects.

Original budget – The first complete appropriated budget. The original budget may be adjusted by reserves, transfers, allocations, supplemental appropriations, and other legally authorized legislative and executive changes before the beginning of the fiscal year. The original budget should also include actual appropriation amounts automatically carried over from prior years by law.

Working capital budget – Combines flexible and fixed budget elements in one document for enterprise and internal service funds. Current operations are flexibly budgeted based on the estimated level of services to be provided and long-range sources and uses of assets are controlled by annual/biennial appropriations and continuing appropriations.

2 Budgeting

2.4 Budget Compliance

2.4.3 Budget Adoption and Amendments

2.4.3.10 All taxing districts must file certified levies and budgets with the county per RCW 84.52.020. All taxing districts are required to hold a public hearing on the proposed levy and budget (excluding capital, enterprise, and special-assessment funds) and adopt their levy by ordinance or resolution per RCW 84.55.120.

2.4.3.20 Additional specific requirements for local governments that are required to expend within their budget are as follows:

2.4.3.30 Requirements for local governments that are not limited to expenditures within their budget are as follows:

Budget amendments

2.4.3.40 For governmental funds (except those types specifically identified above in 2.4.3.30), budgeted appropriations are legally binding. This means that the government cannot spend more than the amount budgeted. As new information becomes available throughout the year, the government can amend (increase) the budget through formal processes. Budget compliance is determined at the end of the fiscal period. Therefore, amendments may be done at any time during the fiscal period, but cannot be done after the fiscal period. If the entity adopts a biennial budget, amendments may be made at any time during the biennium. Regardless, budgetary authority must be in place before actual expenditures are made.

The following local governments have specific requirements for adoption of supplemental budgets:

2 Budgeting

2.4 Budget Compliance

2.4.2 Budget Process

2.4.2.10 The budgetary process encompasses a number of different activities and decisions over a period of several months. See the budget calendar below for cities and counties. Similar steps can be used to develop all types of budgets.

|

BUDGET CALENDAR |

|||

|

Steps in Budget Preparation |

Cites |

Counties |

|

|

1 |

BUDGET ESTIMATES Department heads are requested by clerk to prepare estimates of revenue and expenditures for the next fiscal year. |

On or before the second Monday of the fourth month prior to the beginning of the city's/town's next fiscal year (i.e., September). |

On or before the second Monday in July. |

|

|

|

RCW 35.33.031 (2nd, 3rd, towns, 1st class |

RCW 36.40.010 |

|

|

|

RCW 35.34.050 (Biennial Budgets) |

|

|

|

|

RCW 35A.33.030 (Code Cities) |

|

|

|

|

RCW 35A.34.050 (Code Cities - Biennial Budgets) |

|

|

2 |

BUDGET ESTIMATES Estimates are to be filed with the city clerk/county auditor. |

On or before the fourth Monday in September. |

On or before the second Monday in August. |

|

|

|

RCW 35.33.031 (2nd, 3rd, towns, 1st class |

|

|

|

|

RCW 35.34.050 (Biennial Budgets) |

RCW 36.40.010 |

|

|

|

RCW 35A.33.030 (Code Cities) |

|

|

|

|

RCW 35A.34.050 (Code Cities - Biennial Budgets) |

|

|

3 |

PROPOSED PRELIMINARY BUDGET Estimates are presented to the chief administrative officer for modification, revision, or additions. |

On or before the first business day in October. |

County auditor or chief financial officer shall prepare the county budget. |

|

|

|

RCW 35.33.051 (2nd, 3rd, towns, 1st class |

RCW 36.40.040 |

|

|

|

RCW 35.34.070 (Biennial Budgets) |

|

|

|

|

RCW 35A.33.050 (Code Cities) |

|

|

|

|

RCW 35A.34.070 (Code Cities - Biennial Budgets) |

|

|

4 |

PRELIMINARY BUDGET Chief administrative officer provides the legislative body with: |

(a) Revenue estimates (setting of levies) due no later than the first Monday in October. |

(a) Revenue estimates are part of the preliminary budget process and due when preliminary budget is due. See next section. |

|

|

(a) Estimates of revenues (setting of levies), |

RCW 35.33.135 (2nd, 3rd, towns, 1st class |

|

|

|

|

RCW 35.34.230 (Biennial Budgets) |

|

|

|

|

RCW 35A.33.135 (Code Cities) |

|

|

|

|

RCW 35A.34.230 (Code Cities - Biennial Budgets) |

|

|

|

(b) Clerk's proposed preliminary budget, and |

(b) Preliminary budget at least 60 days before the beginning of the next fiscal year and, |

(b) Preliminary budget submitted by the auditor to the Board of County Commissioners on or before the 1st Tuesday in September for adoption of the preliminary budget. |

|

|

(c) Copies of the preliminary budget are made available to the public. |

(c) Copies are made available to the public not later than six weeks before the beginning of the city's next fiscal period. |

(c) Copies of the preliminary budget are available to the public not later than two weeks immediately preceding the first Monday in October. |

|

|

|

RCW 35.33.055 (2nd, 3rd, towns, 1st class |

|

|

|

|

RCW 35.34.080 (Biennial Budgets) |

|

|

|

|

RCW 35A.33.052 (Code Cities) |

|

|

|

|

RCW 35A.34.080 (Code Cities - Biennial Budgets) |

|

|

5 |

NOTICE OF PUBLIC HEARING Clerk publishes notice of filing of preliminary budget with city clerk and publishes notice of public hearing on final budget once a week for two consecutive weeks. |

Published no later than the first two weeks in November. |

Notice shall be published once each week for two consecutive weeks immediately following adoption of the preliminary budget. |

|

|

|

RCW 35.33.061 (2nd, 3rd, towns, 1st class |

RCW 36.40.060 |

|

|

|

RCW 35.34.100 (Biennial Budgets) |

|

|

|

|

RCW 35A.33.060 (Code Cities) |

|

|

|

|

RCW 35A.34.100 (Code Cities - Biennial Budgets) |

|

|

6 |

PUBLIC HEARING Budget hearing is held. |

On or before the first Monday of December, and may be continued from day to day but not later than the 25th day prior to the commencement of the new fiscal year. |

On the first Monday in October. |

|

|

|

RCW 35.33.071 (2nd, 3rd, towns, 1st class |

RCW 36.40.070 |

|

|

|

RCW 35.34.110 (Biennial Budgets) |

|

|

|

|

RCW 35A.33.070 (Code Cities) |

|

|

|

|

RCW 35A.34.110 (Code Cities - Biennial Budgets) |

|

|

7 |

FINAL BUDGET Adoption of budget for next fiscal year. |

Following the conclusion of the hearing and prior to the beginning of the fiscal year, the legislative body shall by ordinance adopt the budget in its final form. |

At the conclusion of the budget hearing, the county legislative authority shall by resolution adopt the budget. |

|

|

|

A copy of the finalized budget must be sent to the Association of Washington Cities. |

A copy of the finalized budget must be sent to the State Auditor's Office. |

|

|

|

RCW 35.33.075 (2nd, 3rd, towns, 1st class |

RCW 36.40.080 |

|

|

|

RCW 35.34.120 (Biennial Budgets) |

|

|

|

|

RCW 35A.33.075 (Code Cities) |

|

|

|

|

RCW 35A.34.120 (Code Cities - Biennial Budgets) |

|

Which funds need budgets?

2.4.2.20 Generally, all governmental funds including the general fund (also called the current expense fund) and special revenue funds of a local government must have annual/biennial appropriated budgets. Most debt service and capital project fund budget requirements are met by the continuing appropriation contained in the enabling legislation. These funds may not need annual/biennial appropriated budgets.

2.4.2.30 Expenses of proprietary, internal service and fiduciary funds are not considered to be appropriations and therefore are only subject to budgeting requirements as required by the government’s policy.

2.4.2.40 Fiduciary and permanent funds are subject to the trust agreement and their use is restricted by such.

2.4.2.50 Local governments may separately account for different aspects of a legal fund in several “sub-funds” on their general ledger for managerial purposes and roll-up these funds for financial reporting purposes. The minimum level of detail for budget purposes is the legal fund level.

2.4.2.60 Budgeted expenditures (or estimated expenses) should be limited to the amount of budgeted revenues plus the beginning fund balance. Governments are not authorized to appropriate (or estimate) more resources for expenditures than are available. Note that this requirement only applies at the legal fund level. Entities may budget a negative fund balance for departments, programs or sub-funds so long as the combined fund balance for the legal fund is positive.

What constitutes appropriations?

2.4.2.70 All final amounts budgeted as expenses, expenditures, transfers and other financing uses for a fund or department is the appropriation. The government cannot legally exceed this amount. Ending fund balance and nonrevenues (BARS 508 and 58X, if shown on the budget) would not be considered an appropriation. Only line items shown as expenditures (BARS 51X-57X and 59X) would be considered appropriations.

3 Accounting

3.1 Accounting Principles and Internal Control

3.1.10 Accounting Principles

3.1.10.10 The following principles of accounting and financial reporting are based on those set forth in the Governmental Accounting Standards Board’s (GASB) Codification of Governmental Accounting and Financial Reporting Standards (Cod.). The BARS manual permits accounting and financial reporting that conforms to these principles in all respects and requires GAAP municipalities to account and report in conformity with these principles, except that the annual report required is not as extensive as the Annual Comprehensive Financial Report (ACFR).

3.1.10.30 Measurement focus and basis of accounting in the basic financial statements - Government-wide financial statements

The government-wide statement of net position and statement of activities should be prepared using the economic resources measurement focus and the accrual basis of accounting. Revenues, expenses, gains, losses, assets, and liabilities resulting from exchange and exchange-like transactions should be recognized when the exchange takes place. Revenues, expenses, assets, and liabilities resulting from nonexchange transactions should be recognized in accordance with the GASB Cod. Section (Sec.) N50 – “Nonexchange Transactions”.

3.1.10.40 Measurement focus and basis of accounting in the basic financial statements - Fund financial statements

In fund financial statements, the modified accrual or accrual basis of accounting, as appropriate, should be used in measuring financial position and operating results.

a. Financial statements for governmental funds should be presented using the current financial resources measurement focus and the modified accrual basis of accounting. Revenues should be recognized in the accounting period in which they become available and measurable. Expenditures should be recognized in the accounting period in which the fund liability is incurred, if measurable, except for unmatured interest on general long-term liabilities, which should be recognized when due.

b. Proprietary fund statements of net position and revenues, expenses, and changes in fund net position should be presented using the economic resources measurement focus and the accrual basis of accounting.

c. Financial statements of fiduciary funds should be reported using the economic resources measurement focus and the accrual basis of accounting, except for the recognition of certain liabilities of defined benefit pension plans and certain postemployment healthcare plans. Additionally, governments should review assets received or disbursements made soon after the end of a fiscal year to evaluate the need for accruals in the fiduciary funds.

d. Transfers should be reported in the accounting period in which the interfund receivable and payable arise.

Note: The various fund types may be grouped in the following manner to more clearly portray their relationship to an accounting basis:

Flow of Current Financial Resources Measurement Focus Funds – use the modified accrual basis:

000-099: General (Current Expense) Fund

100-199: Special Revenue Funds

200-299: Debt Service Funds

300-399: Capital Projects Funds

700-799: Permanent Funds

Flow of Economic Resources Measurement Focus Funds – use full-accrual basis:

400-499: Enterprise Funds

500-599: Internal Service Funds

600-609: Investment Trust Funds

610-619: Pension (and Other Employee Benefit) Trust Funds

620-629: Private-Purpose Trust Funds

630-698: Custodial Funds

699: External Investment Pool Fund

3.1.10.50 Reporting capital assets

A clear distinction should be made between general capital assets and capital assets of proprietary and fiduciary funds. Capital assets of proprietary funds should be reported in both the government-wide and fund financial statements. Capital assets of fiduciary funds should be reported only in the statement of fiduciary net position. All other capital assets of the government are general capital assets. They should not be reported as assets in governmental funds but should be reported in the governmental activities column in the government-wide statement of net position. The Capital Assets (BARS BARS 3.3.9, 3.3.10 and 3.3.11) sections of the BARS manual provide additional information regarding accounting and reporting of capital assets.

3.1.10.60 Reporting long-term liabilities

A clear distinction should be made between fund long-term liabilities and general long-term liabilities. Long-term liabilities directly related to and expected to be paid from proprietary funds should be reported in the proprietary fund statement of net position and in the government-wide statement of net position. Long-term liabilities directly related to and expected to be paid from fiduciary funds should be reported in the statement of fiduciary net position. All other unmatured general long-term liabilities of the governmental unit should not be reported in governmental funds but should be reported in the governmental activities column in the government-wide statement of net position.

3.1.10.70 Revenue, expenditures, expense and transfer account classifications

a. At a minimum, the statement of activities should present:

(1) Activities accounted for in governmental funds by function to coincide with the level of detail required in the governmental fund statement of revenues, expenditures, and changes in fund balances

(2) Activities accounted for in enterprise funds by different identifiable activities.

(3) Contributions to term and permanent endowments, contributions to permanent fund principal, other capital contributions, special and extraordinary items, and transfers between governmental and business-type activities should each be reported separately from, but in the same manner as, general revenues.

b. In governmental fund statement of revenues, expenditures, and changes in fund balances:

(1) Revenues should be classified by fund and source. Expenditures should be classified by fund, function (or program), organization unit, activity, character, and principal classes of objects.

(2) Proceeds of general long-term debt issues should be classified separately from revenues and expenditures.

(3) Transfers should be classified separately from revenues and expenditures

(4) Special and extraordinary items should be reported separately after “other financing sources and uses”.

c. In proprietary fund statement of revenues, expenses, and change in fund net position should present:

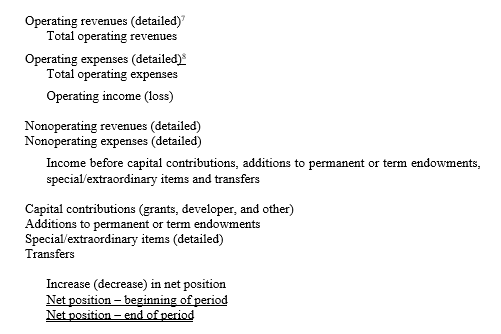

(1) Revenues should be reported by major sources and expenses should be classified in essentially the same manner as those of similar business organizations, functions, or activities. Revenues and expenses should be distinguished as operating and nonoperating.

(2) Contributions to term and permanent endowments, other capital contributions, and special and extraordinary items should be reported separately after nonoperating revenues and expenses.

(3) Transfers should be reported after nonoperating revenues and expenses.

3.1.10.75 Reimbursements from external parties

Corrections of an error, receipt of a refund for an expense/expenditure (example: returning a supply or cancelling a training class), or the receipt of a vendor discount/rebate awarded after the transaction is completed would qualify as reimbursement and as such, they should be treated in similar manner like interfund reimbursements, see BARS 3.9.4, Interfund Reimbursements. If a local government has an ongoing relationship with an external entity (e.g., phone company, etc.) the amounts of reimbursements most likely would be included in the upcoming bill, so no adjusting entry is required. If the reimbursement is related to the expense/expenditure from the previous fiscal year and is immaterial, the amount of reimbursement should be recorded as revenue. If it is material, the government should record the reimbursement as an error correction, see BARS 3.1.10.100 below.

Examples of transactions that should not be accounted for as reimbursements include: state payments for public health services, expert witnesses, police salaries while attending criminal justice training; federal/state/local payments for the care and custody of prisoners and for election costs; local payments for data processing services, police/sheriff services, street maintenance, etc.; private payments for street repairs, culvert installations, weed control, demolition of dangerous property, subleases, etc.

3.1.10.80 Annual financial reports

The items listed below and in BARS 4.1.1, GAAP Reporting Requirements follow national standards of financial reporting. They should not be confused with legal reporting requirements, which are prescribed by the State Auditor’s Office for all local governments in Washington State. The legal requirements are consistent with these national standards, but they are not identical. Specific legal reporting requirements can be found in BARS 4.1.2, BARS Reporting Requirements.

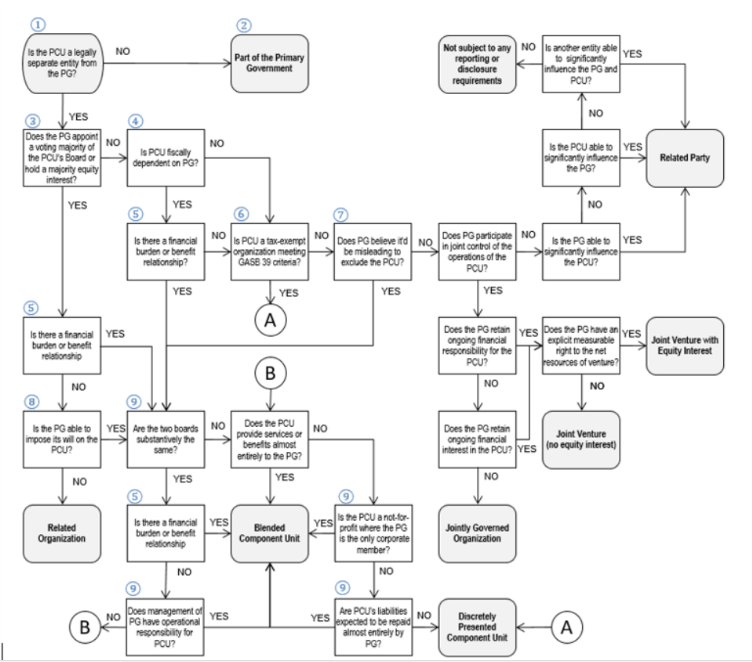

The financial statements should include the financial reporting entity which consists of (1) the primary government, (2) organizations for which the primary government is financially accountable, and (3) other organizations for which the nature and significance of their relationship with the primary government are such that exclusion would cause the reporting entity’s basic financial statements to be misleading or incomplete. For more information see BARS 4.1.1, GAAP Reporting Requirements.

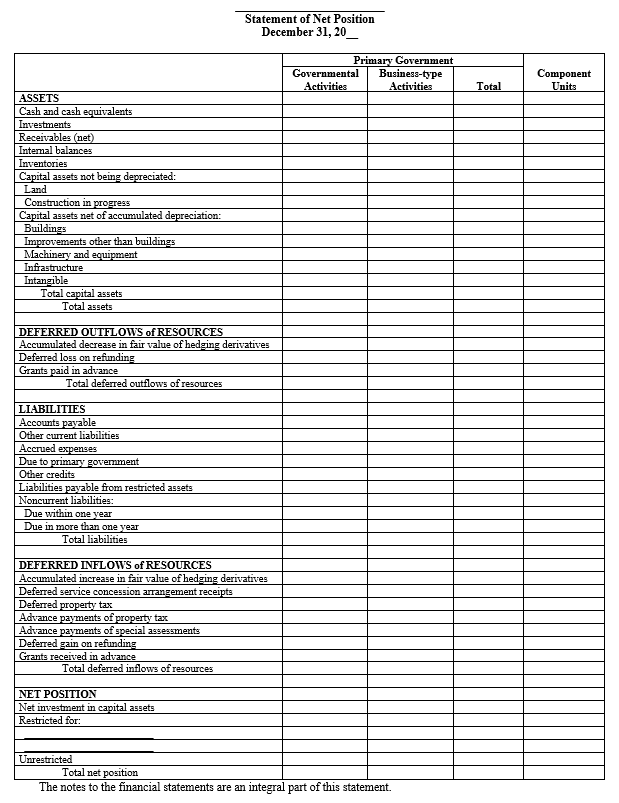

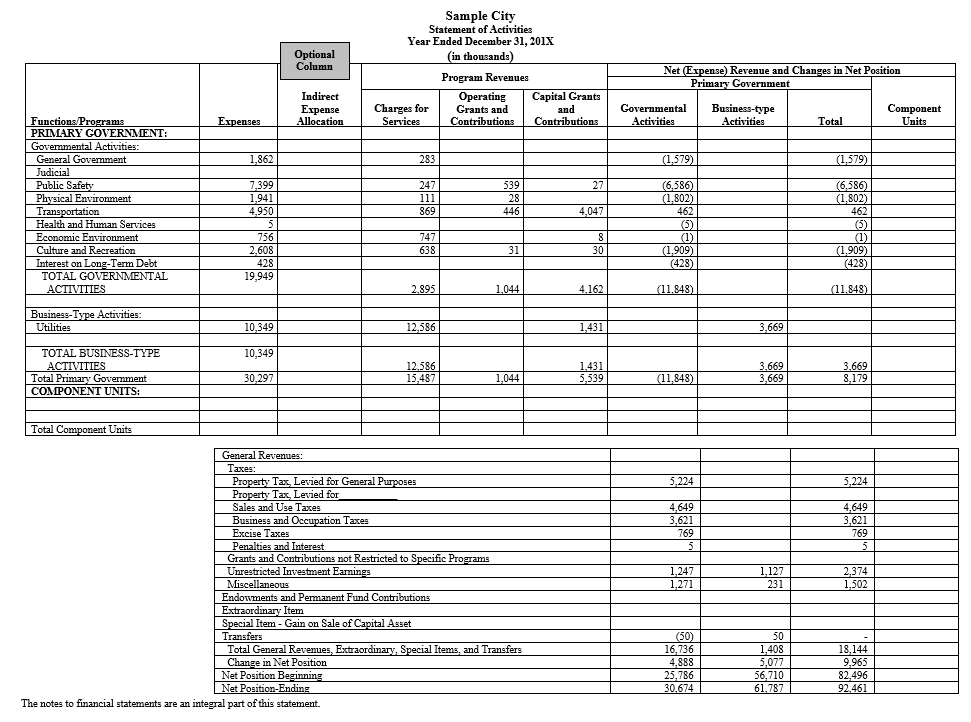

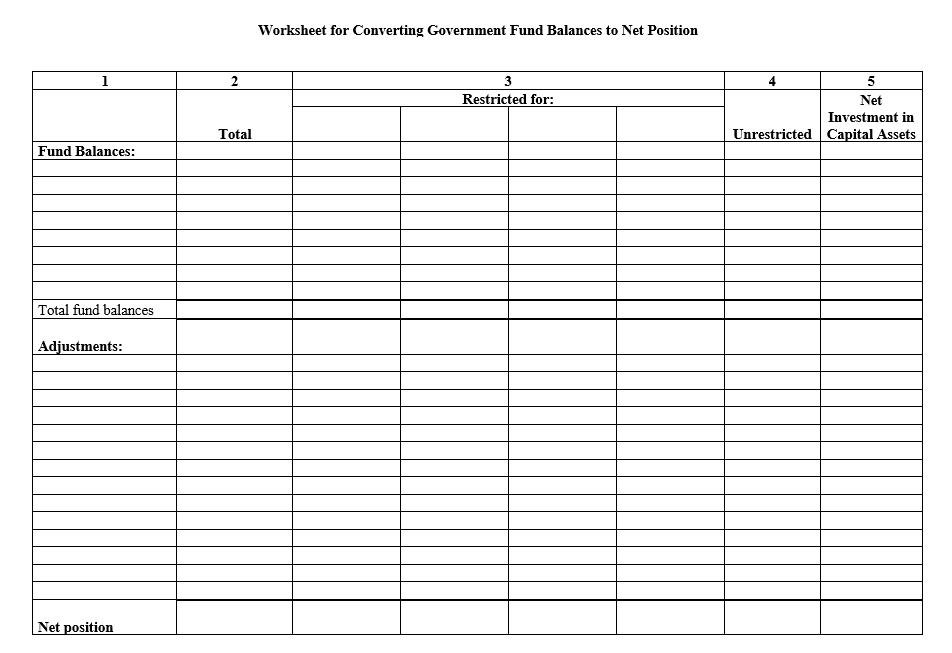

a. General purpose external financial reports should be prepared and published. Governments engaged in governmental and business-type activities should include, at a minimum:

(1) Management’s discussion and analysis (MD&A).

(2) Basic financial statements. The basic financial statements should include:

(a) Government-wide financial statements.

(b) Fund financial statements.

(c) Notes to the financial statements.

(3) Required supplementary information (RSI) other than MD&A.

b. Governments engaged only in business-type activities should present only the financial statements required for proprietary funds. They should include:

(1) Management’s discussion and analysis (MD&A)

(2) Proprietary fund financial statements

(3) Notes to the financial statements

(4) Required supplementary information (RSI) other than MD&A, if applicable.

An Annual Comprehensive Financial Report (ACFR) may be prepared and published covering all activities of the financial reporting entity. The ACFR includes not only the financial reports listed above but also an introductory section, combining and individual fund statements, schedules, narrative explanations, and a statistical section. Preparation of an ACFR is not required.

3.1.10.90 Accounting changes and error corrections - Definitions

The GASB Cod. Sec. 2250 "Additional Financial Reporting Considerations" establishes standards of accounting and reporting regarding accounting changes and error corrections.

There are four categories of accounting changes and error corrections defined as follows:

Change in accounting principle:

A change in accounting principle is the application of an accounting principle to transactions, or events, of similar type that is different than the accounting principle previously applied.

A change occurs when:

a. A change in the application of one generally accepted accounting principle to another that is justified on the basis that the new one is preferable

b. The implementation of new pronouncements

Change in accounting estimate:

An accounting estimate is an amount subject to measurement uncertainty that is calculated based on inputs and disclosed in the basic financial statements. Inputs can be data, assumptions, or measurement methodologies.

A change in accounting estimate occurs when the inputs (which could be a change to data, assumptions, or measurement methodologies) used to calculate the accounting estimate have changed. Changes may result from a change in circumstances, new information or more experience.

Change to or within the financial reporting entity:

A change to or within the financial reporting entity occurs when the any of the following occur:

a. The addition or removal of a fund that results from the movement of continuing operations within the primary government, including its blended component units

b. A change in a fund’s presentation from major or nonmajor

c. The addition/removal of a component unit to the financial reporting entity

d. There is a change in a component unit’s presentation as blended or discretely presented

Error correction:

An error occurs when any of the following are identified as of the previous financial statement date:

a. Mathematical mistake

b. Mistake in the application of accounting principles

c. Oversight or misuse of facts that existed at the time the financial statements were issued about conditions that existed as of the financial statement date is identified.

3.1.10.100 Accounting changes and error corrections - Accounting and reporting

Accounting and reporting for each accounting change and error correction category is discussed below. If a government has separately displayed in the financial statements the effects of each accounting change or error correction by reporting unit, those effects need not be repeated in the notes to the financial statements. Additionally, note disclosure requirements for each accounting change and error correction can be found at Note X - Accounting Changes and Error Corrections.

Change in accounting principle:

In the absence of other specific guidance, governments that experience a change in accounting principle should report the change retroactively by restating the beginning net position, fund balance, or fund net position by the cumulative effect of the change on prior periods.

Change in accounting estimate:

Governments that experience a change to an accounting estimate calculation should recognize the change prospectively in the reporting period that the change occurs, unless other specific requirements address how a change would be reported.

Change to or within the financial reporting entity:

Governments that experience a change to or within the financial reporting entity should recognize the change by adjusting the current period beginning net position, fund balance or fund net position. The recognition of this will appear as if the change occurred at the beginning of the reporting period.

Error correction:

In the case that a government is required to correct an error, the correction should be reported retroactively by restating the financial statements for all periods presented. The restatement amount should total the cumulative effect of the error on the net position, fund balance or fund net position impacted by the error.

For guidance on how to apply accounting changes and error corrections to comparative financial statements, see GASB Cod. Sec. 2250.

3.1.10.110 Accounting changes and error corrections - Required Supplementary Information (RSI) and Supplementary Information (SI)

Change in accounting principle and to or within the financial reporting entity

For reporting periods that are presented in the basic financial statements, the same periods presented in required supplementary information (RSI) (including management’s discussion and analysis [MD&A]) or supplementary information (SI) should be consistent with the manner in which the information for those periods is presented in the basic financial statements. (That is, the reporting periods should be adjusted or restated in the same manner as the basic financial statements.)

For prior reporting periods that are earlier than those presented in the basic financial statements, information for those prior periods that is presented in RSI (including MD&A) or SI should not be restated for a change in accounting principles or a change to or within the financial reporting entity.

If prior-period information presented in RSI (including MD&A) or SI is not consistent with current-period information as a result of a change in accounting principle or a change to or within the financial reporting entity, an explanation of why the information is not consistent should be provided in RSI (including MD&A) or SI, as applicable. In MD&A, that explanation should include a reference to the related note disclosure in the basic financial statements.

Error correction

For reporting periods that are presented in the basic financial statements, the same periods presented in RSI (including MD&A) or SI should be restated. If the error affects periods earlier than those presented in the basic financial statements, all affected information should be corrected by restating the information for those prior periods in RSI (including MD&A) or SI, if practicable.

Information presented in RSI (including MD&A) or SI that is affected by an error should be identified as restated or not restated, as appropriate, and an explanation about the nature of the error should be provided in RSI (including MD&A) or SI, as applicable.

In addition, if it is not practicable to restate information in RSI or SI in the reporting year of the error correction, an explanation of why it is not practicable to restate should be provided in RSI (including MD&A) or SI, as applicable. It is expected that the restatement of the RSI and SI will be performed in the next reporting period’s financial statements.

3 Accounting

3.1 Accounting Principles and Internal Controls

3.1.1 Fund Accounting and Fund Types

3.1.1.10 The following principles of accounting and financial reporting are based on those set forth in the Governmental Accounting Standards Board’s (GASB) Codification of Governmental Accounting and Financial Reporting Standards (Cod). The BARS manual permits accounting and financial reporting that conforms to these principles in all respects and requires GAAP municipalities to account and report in conformity with these principles, except that the annual report required is not as extensive as the Annual Comprehensive Financial Report (ACFR).

3.1.1.20 Accounting and reporting capabilities

A governmental accounting system must make it possible both: (a) to present fairly and with full disclosure the funds and activities at the government in conformity with generally accepted accounting principles; and (b) to determine and demonstrate compliance with finance-related legal and contractual provisions.

3.1.1.30 Fund accounting systems

A governmental accounting system should be organized and operated on a fund basis. A fund is defined as a fiscal and accounting entity with a self-balancing set of accounts recording cash and other financial resources, together with all related liabilities and residual equities or balances, and changes therein, which are segregated for the purpose of carrying on specific activities or attaining certain objectives in accordance with special regulations, restrictions, or limitations. Fund financial statements should be used to report detailed information about the primary government, including its blended component units. The focus of governmental and proprietary fund financial statements is on major funds.

3.1.1.40 Types of funds

In fund financial statements, governments should report governmental, proprietary, and fiduciary funds to the extent that they have activities that meet the criteria for using these funds.

Presented below is a system to classify all funds used by local government and the assignment of code numbers to identify each type of fund. A three-digit code is used: the first digit identifies the fund type, and the next two digits will be assigned by the governmental unit to identify each specific fund.

Since counties account for special purpose districts in their accounting systems as fiduciary funds, they often provide the districts with reports showing assigned fund codes 630-699. These codes refer to the fund from the county perspective. A district has to “reassign” the county code to the code appropriate to the fund type it is reporting (e.g., if the district’s general fund is coded in the county records as 663, the district in its annual report has to code this fund as 001).

For reporting purposes local governments are required to follow the fund structure described below. However, the local governments may create other funds for accounting or managerial purposes. When preparing external financial reports, those funds should be rolled to appropriate fund types as discussed at BARS 3.1.12, Managerial Funds.

Governmental funds

Code 000 - General (Current Expense) Fund – should be used to account for and report all financial resources not accounted for and reported in another fund.

Although a local government has to report only one general fund in its external financial reports, the government can have multiple general subfunds for its internal managerial purposes. These funds should follow guidance found at BARS 3.1.12, Managerial Funds.

Code 100 - Special Revenue Funds – are used to account for and report the proceeds of specific revenue sources that are restricted or committed to expenditures for specific purposes other than debt service or capital projects. Restricted revenues are resources externally restricted by creditors, grantors, contributors or laws or regulations of other governments or restricted by law through constitutional provisions or enabling legislation (similar to the restricted component of net position used in government-wide reporting). Committed revenues are resources with limitations imposed by the highest level of the government, and where the limitations can be removed only by a similar action of the same governing body. Revenues do not include other financing sources (long-term debt, transfers, etc.).

The term proceeds of specific revenue sources establishes that one or more specific restricted or committed revenues should be the foundation for a special revenue fund. They should be expected to continue to comprise a substantial portion of the inflows reported in the fund. While GASB Cod. Section (Sec.) 1300 "Fund Accounting" has not provided a numeric range for substantial portion of inflows, it was recommended that at least 20 percent is a reasonable limit for reporting a special revenue fund. Local governments need to consider factors such as past resource history, future resource expectations and unusual current year inflows such as debt proceeds in their analysis.

They may use the calculation below to determine whether an activity would qualify for reporting as a special revenue fund.

|

Substantial portion of inflows = |

(restricted revenues + committed revenues) |

|

total resources* reported in the fund |

*Total resources would include all revenues and other financing sources.

Other resources (investment earnings and transfers from other funds, etc.) also may be reported in the fund if these resources are restricted, committed, or assigned to the specific purpose of the fund.

Governments should discontinue reporting a special revenue fund, and instead report the fund’s remaining resources in the general fund, if the government no longer expects that a substantial portion of the inflows will derive from restricted or committed revenue sources.

Codification requires all revenue to be recognized in the special revenue fund. If the resources are initially received in another fund, such as the general fund, and subsequently remitted to a special revenue fund, they should not be recognized as revenue in the fund initially receiving them. They should be recognized as revenue in the special revenue fund from which they will be expended.

Special revenue funds should not be used to account for resources held in trust for individuals, private organizations, or other governments.

The general fund of a blended component unit should be reported as a special revenue fund.

The state statutes contain many requirements for special funds to account for different activities. The legally required funds do not always meet GAAP standards for external reporting. So, while the local governments are required to follow their legal requirements, they will have to make some adjustment to their fund structure for external financial reporting.

Code 200 - Debt Service Funds – may be used to account for and report financial resources that are restricted, committed, or assigned to expenditure for principal and interest. Debt service funds should be used to report resources if legally mandated. Financial resources that are being accumulated for principal and interest maturing in future years also should be reported in debt service funds. The debt service transactions for a special assessment for which the government is not obligated in any matter should be reported in a custodial fund. Also, if the government is authorized, or required to establish and maintain a special assessment bond reserve, guaranty, or sinking fund, GASB Cod. Sec. S40 "Special Assessments" requires using a debt service fund for this purpose.

Note: Debt service funds should not be used in proprietary funds (400 and 500). Use enterprise funds (400) or internal service (500) for debt payments related to utilities and other business type activities.

Code 300 - Capital Projects Funds – may be used to account for and report financial resources that are restricted, committed, or assigned to expenditure for capital outlays including the acquisition or construction of capital facilities or other capital assets. Capital outlays financed from general obligation bond proceeds should be accounted for through a capital projects fund. Capital project funds exclude those types of capital-related outflows financed by proprietary funds or for assets that will be held in trust for individuals, private organizations, or other governments (private-purpose trust funds).

Note: Capital project funds should not be used in proprietary funds (400 and 500). Use enterprise funds (400) or internal service (500) for capital payments related to utilities and other business type activities.

Code 700 - Permanent Funds – should be used to account for and report resources that are restricted to the extent that only earnings, and not principal, may be used for purposes that support the reporting government’s programs – that is for the benefit of the government or its citizens (public-purpose).

Permanent funds are required to have a nonspendable fund balance for the principal portion that cannot be spent. Any unspent interest remaining in the fund would be reported under one of the other fund balance classifications, such as restricted.

Generally, only the principal amounts, interest revenue, and transfers to the appropriate operating fund for interest revenue use should be reported in this fund. Note: if the allowable use of the interest earnings is related to operating expenses that are normally reported in another fund, the permanent fund should transfer the allowable amount to the appropriate operating fund.

Permanent funds do not include private-purpose trust funds which account for resources held in trust for individuals, private organizations, or other governments.

Proprietary funds

Code 400 - Enterprise Funds - may be used to report any activity for which a fee is charged to external users for goods or services. Enterprise funds are required for any activity whose principal revenue sources meet any of the following criteria:

These criteria should be applied in the context of the activity’s principal revenue source.