Note X – Long-Term Debt

A. Long-Term Debt

The (city/county/district) issues general obligation and revenue bonds to finance the purchase of __________ and the acquisition or construction of __________. Bonded indebtedness has also been entered into (currently and in prior years) to advance refund several general obligation and revenue bonds. General obligation bonds have been issued for both general government and business-type activities and are being repaid from the applicable resources. The revenue bonds are being repaid by proprietary fund revenues. The (city/county/district) is also liable for notes that were entered into for the purchase of __________. These notes are considered obligations of the general government and are being repaid with general governmental revenue sources.

General obligation bonds currently outstanding are as follows: [1]

The annual debt service requirements to maturity for general obligation bonds are as follows:

Also see Footnote 2

The annual debt service requirements to maturity for debt from direct borrowings and direct placement are as follows:

Also see Footnote 2

The revenue bonds currently outstanding are as follows: [1]

Revenue bond debt service requirements to maturity are as follows:

Also see Footnote 2

In proprietary funds, unamortized debt issue costs for insurance are recorded as an asset and bonds are displayed net of premium or discount; annual interest expense is decreased by amortization of debt premium and increased by the amortization of debt issue costs and discount. [3]

At December 31, 20__, the (city/county/district) has $__________ available in debt service funds to service the general bonded debt. Restricted assets in proprietary funds contain $__________ in sinking funds and reserves as required by bond indentures.

The (city/county/district) has pledged future (identify pledged revenue) revenue, net of (e.g., specified operating expenses, etc.), to repay $ in revenue bonds issued in , 20__. Proceeds from the bonds provided financing for (describe the purpose). The bonds are payable solely from (identify pledged revenue) revenue and are payable through 20__. Annual principal and interest payments on the bonds are expected to require less than percent of net revenues. The total principal and interest remaining to be paid on the bonds is $ . Principal and interest paid for the current year and total (identify pledged revenue) were $ and $ , respectively. [4]

B. Refunded Debt [5]

The (city/county/district) issued $__________ of general obligation refunding bonds to provide resources to purchase U.S. Government and State and Local Government Series securities that were placed in an irrevocable trust for the purpose of generating resources for all future debt service payments on $__________ of refunded debt. As a result, the refunded bonds are considered to be defeased and the liability has been removed from the governmental activities column of the statement of net position. This advance refunding was undertaken to reduce total debt service payments over the next _____ years by $__________ and resulted in an economic gain of $__________.

Debt service requirements to maturity that would result if the take-out agreement were exercised

C. Conduit Debt [6]

D. Special Assessments [7]

E. Demand Bonds [8]

F. Unused Lines of Credit

The (city/county/district) also has an outstanding line of credit in the amount of $_____.

G. Other [9]

Instructions to preparer:

If conduit (no-commitment) debt is reported on the balance sheet, it needs to be included in all long-term disclosures.

Include all of the Schedule of Liabilities (Schedule 09), except debt of special purpose districts accounted for by counties.

If the city/county/district is authorized to issue debt that has not yet been issued, the notes should disclose this fact.

[1] The interest for variable-rate debt should be computed using rate effective at year end. The government should also disclose the terms by which interest rates for variable-debt change.

This disclosure is recommended. Also, it’s recommended to disclose applicability of federal arbitrage regulations.

[2] Use five-year increments thereafter.

[3] If the government displays general long-term or special assessment debt net of premium or discount, you need to modify this paragraph to disclose the government’s policy. You need to make a similar disclosure if the government capitalizes debt issue costs (rather than showing them as a current expenditure when paid, or netting proceeds of long-term debt) for general debt.

[4] For more details see Governmental Accounting Standards Board (GASB) Statement 48, Sales and Pledges of Receivables and Future Revenues and Intra-Entity Transfer of Assets and Future Revenues, paragraph 21.

The disclosures in this paragraph are not required for legally separate entities that report as stand-alone business-type activities whose operations are financed primarily by a single major revenue source.

If a specific revenue stream is pledged as security for multiple debt issuances, the required disclosures may be combined in a single note.

For this disclosure, pledged revenues recognized during the period may be presented net of specified operating expenses, based on the provisions of the pledged agreement; however, the amounts should not be netted in the financial statements.

[5] The city/county/district that issues debt to defease or otherwise extinguish existing obligations should provide this disclosure in the year of transaction. In the periods following an advance refunding in which the old debt is still outstanding the city/county/district would make the following disclosure:

In prior years the (city/county/district) defeased certain general obligation bonds by placing the proceeds of new bonds in an irrevocable trust to provide for all future debt service payments on the old bonds. Accordingly, the trust account assets and the liability for defeased bonds are not included in the (city/county/district's) financial statements. At December 31, 20___, $__________ (*) of bonds outstanding are considered defeased.

(*) The amount should include debt refunded with resources other than refunding debt (GASB Statement 86, Certain Debt Extinguishment Issues).

The economic gain or loss on a refunding transaction is calculated in the following manner:

-

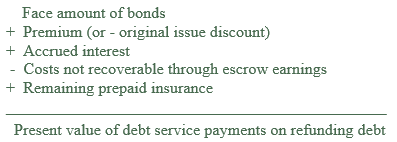

The present value of the debt service payments related to the refunding debt is calculated using the following formula:

-

A calculation is made to determine what effective interest rate applied to the debt service payments on the refunding bonds would result in the present value determined in the previous calculation;

-

The effective interest rate calculated for the refunding bonds is then applied to the debt service on the refunded bonds to calculate the present value of debt service on the latter;

-

The difference between the present value of the two debt service streams (refunding debt and refunded debt) constitutes the economic gain or loss on the transaction.

If the government is using only existing resources, the note should include a general description of the transaction (e.g., amount of debt, amount of cash and other monetary assets acquired with existing resources placed with the escrow agent, the reasons for defeasance, the cash flows required to service the defeased debt, etc.).

The government should also disclose, if applicable, a lack of a prohibition in substituting essentially risk-free monetary assets with monetary assets that are not essentially risk-free. In the following periods, the amounts outstanding for which there is no prohibition in a substitution should be reported separately. (GASB Statement 86, Certain Debt Extinguishment Issues)

The city/county/district should disclose: amounts of debt defeased in substance, but still outstanding as of the end of each fiscal year, should be disclosed in the notes. The amount should include debt refunded with resources other than refunding debt (GASB Statement 86, Certain Debt Extinguishment Issues)

[6] See BARS Manual 3.4.12, Financial Guarantees and Conduit Debt for information on conduit debt.

The city/county/district should disclose:

-

A general description of their conduit debt obligations

-

A general description of their limited commitments

-

A general description of their voluntary commitments (if any)

-

A general description of their additional commitments (if any), including:

-

The legal authority and limits for extending the commitments

-

The length of time of the commitments

-

Arrangements, if any, for recovering payments from the third-party obligors

-

-

The aggregate outstanding principal amount of all conduit debt obligations that share the same type of commitment at the end of the reporting period.

If the city/county/district recognized a liability related to conduit debt they should disclose:

-

A brief description of the timing of recognition and measurement of the liability and information about the changes in the recognized liability, including:

-

Beginning of period balances

-

Increases, including payments made and adjustments increasing estimates

-

Decreases, including payments made and adjustments decreasing estimates

-

End of period balances

-

-

Cumulative amounts of payments that have been made on the recognized liability at the reporting date (if any)

-

Amounts expected to be recovered from those payments (if any).

Additionally, there may be instances in which an issuer’s additional commitment for each individual conduit debt obligation does not meet the recognition criteria, but when all such commitments are considered in the aggregate, it becomes more likely than not that some additional commitment will be honored. In those situations, the issuer may need to consider the disclosure requirements in paragraph 107 of Statement 62, as amended, when no liability is recognized for a loss contingency.

[7] If the city/county district issued a special assessment for which is obligated in some manner, the note should discuss this debt. The note should disclose the nature of the city/county/district’s obligation. It should identify and describe any guarantee, reserve or sinking fund established to cover defaults by property owners. If not discernible on the face of the financial statements, the note should disclose the amount of delinquent special assessments receivable.

If the city/county/district issued a special assessment for which is not obligated in any manner, the note should disclose this debt, amount and the fact that the city/county/district is acting only as an agent and is not liable for debt.

[8] The notes should disclose all of the following information regarding demand bonds:

-

The terms of any letters of credit or other liquidity facilities outstanding,

-

Commitment fees to obtain the letters of credit and any amounts drawn on them outstanding as of the end of the fiscal year,

-

The take-out agreement including its expiration date, commitment fees to obtain that agreement, and the terms of any new obligation incurred or expected to be incurred as a result of the take-out agreement.

[9] Examples:

-

Loans with forgiveness clauses. Include parties in contract, property secured, terms to convert the loan to a grant, amount to be repaid if forgiveness conditions are not met.

-

Grants with recoverable clauses. Include: parties in contract, terms removing recoverable clause, the asset the grantor has an interest in, the amount the grantor can require to be returned, and the conditions that trigger return of the grantor interest.

-

Assets pledged as collateral for debt. Include type and amount of debt which is subject of the collateral (GASB Statement 88, Certain Disclosures Related to Debt, including Direct Borrowings and Direct Placements).

-

Terms specified in debt agreements related to significant (1) events of default with finance-related consequences, (2) termination events with finance-related consequences, and (3) subjective acceleration clauses. (GASB Statement 88, Certain Disclosures Related to Debt, including Direct Borrowings and Direct Placements)